[ad_1]

The logo of Alibaba Group is seen during Alibaba Group’s 11.11 Singles’ Day global shopping festival at the company’s headquarters in Hangzhou, Zhejiang province, China, November 10, 2019. REUTERS/Aly Song

Register now for FREE unlimited access to Reuters.com

HONG KONG, March 23 (Reuters Breakingviews) – In Hans Christian Andersen’s fable, an emperor is swindled into buying “invisible” new clothes until a child points out what fawning courtiers could not admit: the man is walking around naked. Similarly, both Chinese technology giants and their once-enthusiastic investors are waking up to realise how exposed they are after years of flattery and hype.

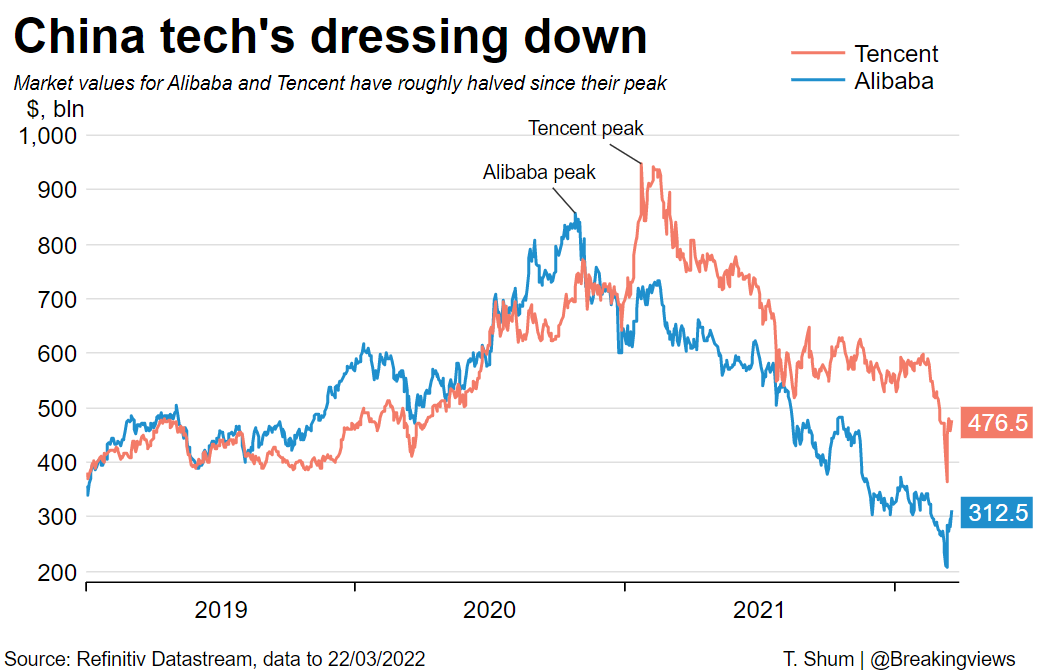

Over the last decade, global funds have thrown money at the country’s internet names on hopes that online spending by China’s rising middle class could compensate for governance red flags, questionable business models and endemic political and regulatory risk. This enthusiasm intensified during the pandemic. From the start of 2019 to mid-February of 2021, the Hang Seng Tech Index (.HSTECH) of major Chinese web firms listed in Hong Kong roughly tripled; heavyweights Tencent (0700.HK) and Alibaba (9988.HK), both of which benefitted from a lockdown-induced boom in e-commerce and video-games, gained a combined $900 billion in market value over the period.

The party was winding down well before Russia invaded Ukraine last month. A targeted campaign against risk in the financial technology sector in late 2020 steadily transformed into an unpredictable and endless series of crackdowns encompassing online tutoring, video-games, cybersecurity and antitrust. read more Outside the country, U.S. authorities are moving towards booting over 200 Chinese companies off New York bourses as a result of a long-running auditing standoff. That threatens to cut off a popular funding channel for unprofitable local startups. And now confidence in China’s zero-tolerance approach to Covid-19 and economic outlook is waning as fresh outbreaks push cities back into lockdown. read more

Register now for FREE unlimited access to Reuters.com

Investors have started bailing out en masse. Even after Chinese regulators reassured the markets last week, setting off a huge relief rally, Hong Kong’s technology index is still down roughly 15% this year, as is the Nasdaq Golden Dragon China Index (.HXC) that tracks New York-listed Chinese firms. Chinese equities are now trading at a more than one-third discount to the rest of the world, according to a Reuters analysis. read more Earlier this month, analysts at J.P. Morgan more than halved their Alibaba share target to $65, below the company’s 2014 initial public offering price, part of a mass downgrade of more than two dozen Chinese internet stocks. The e-commerce giant, which announced a $25 billion share buyback on Tuesday, has shed $545 billion in market value since a 2020 peak.

The correction, combined with the prospect of higher borrowing costs, has investors looking harder at profit margins instead of raw user growth. That is bad news for a lot of Chinese upstarts that focused on grabbing market share quickly with lavish subsidies and acquisitions, assuming profitability would inevitably follow.

Take Alibaba challenger Pinduoduo (PDD.O). The Facebook-meets-Groupon e-commerce darling saw its market value grow nine-fold to over $250 billion in just three years following its 2018 New York debut. But its triple-digit customer and revenue growth rates were largely driven by aggressive sales and marketing; it eked out its first quarterly net profit last June. It has started investing in agriculture, following some peers, but farming seems a dubious path to fat margins. Worse, in the quarter ending in December, Pinduoduo reported that average monthly active users and revenue barely grew from a year earlier. The stock is down some 65% over the past 12 months. Three of the four worst performing large-cap companies over the same period on American exchanges are Chinese technology plays.

Established champions like Alibaba and Tencent have fared better, but they are under increasing pressure to squeeze more out of existing businesses. That’s not easy. Alibaba reported its own metric of adjusted profit margins at its core China business tumbled to 34% in the last quarter of 2021, from 45% a year earlier; Tencent, which is due to report quarterly results on Wednesday, is facing ever-toughening restrictions on its cash-cow video-games business. Food delivery and ride-hailing services from Meituan (3690.HK) and Didi Global (DIDI.N) are under pressure to cap fees and hike wages.

To survive and thrive, China Tech Inc will need to slash costs, offload non-core assets and perhaps restructure business units to hedge against regulatory risks. Alibaba and Tencent are already together preparing to cut tens of thousands of jobs this year, Reuters reported citing sources. read more

Fresh growth might be found in other countries. Tencent’s overseas video-games revenue, for example, is forecast to increase an impressive 18% year-on-year in the three months to December, Citi analysts estimate. But rising suspicion of Chinese companies abroad will continue to complicate offshore expansion plans. Either way, in coming years, China technology’s emperors will need to find a new look to restore market confidence.

Follow @mak_robyn on Twitter

CONTEXT NEWS

– Alibaba on March 22 increased its share buyback programme from $15 billion to $25 billion, effective for two years. As of March 18, the e-commerce champion had spent $9.2 billion under a previously announced share repurchase programme.

– Separately, technology conglomerate Tencent is expected to report revenue of 148 billion yuan ($23.2 billion) in the three months to December, according to the mean analyst forecast compiled by Refinitiv, representing a record low 10.4% increase from a year earlier.

– The company is scheduled to report quarterly results on March 23 after Hong Kong markets close.

Register now for FREE unlimited access to Reuters.com

Editing by Pete Sweeney and Katrina Hamlin

Sign up for a free trial of our full service at https://www.breakingviews.com/trial and follow us on Twitter @Breakingviews and at www.breakingviews.com. All opinions expressed are those of the authors.

[ad_2]

Source link

More Stories

Experts Weigh In On Voice Control Technology’s Pros, Cons And Future

Max Scherzer’s thoughts on PitchCom: ‘It should be illegal’

Coding skills are in demand, but companies want more from technology professionals