[ad_1]

The most critical component of an automobile-loan is arguably the desire fee. It instantly influences the sizing of month to month payments and total bank loan tenor. Desire premiums can even enjoy a job in the ultimate shopping for selection, effective adequate to override sentimental invest in reasons such as brand name loyalty. It goes without expressing, for that reason, that possible vehicle buyers fork out attention to elements that determine their interest rates when searching for vehicle-funding possibilities.

A single of these factors is the credit score. It is essentially a weighted score that tells automobile-lenders how a great deal hazard they are having on by dealing with a future borrower. You most probable have a credit score report if you have any credit score accounts, this sort of as credit history playing cards, home loans or financial loans. This report then types the foundation for identifying your credit rating.

It is not an correct evaluate, but it does get rid of gentle on elements these as the borrower’s willingness and ability to service the personal loan. Simply put, the far better your credit rating score, the increased your likelihood of securing an auto personal loan with favourable curiosity charges. This is significantly vital these days as we navigate the period of fascination charge hikes and inflationary pressures.

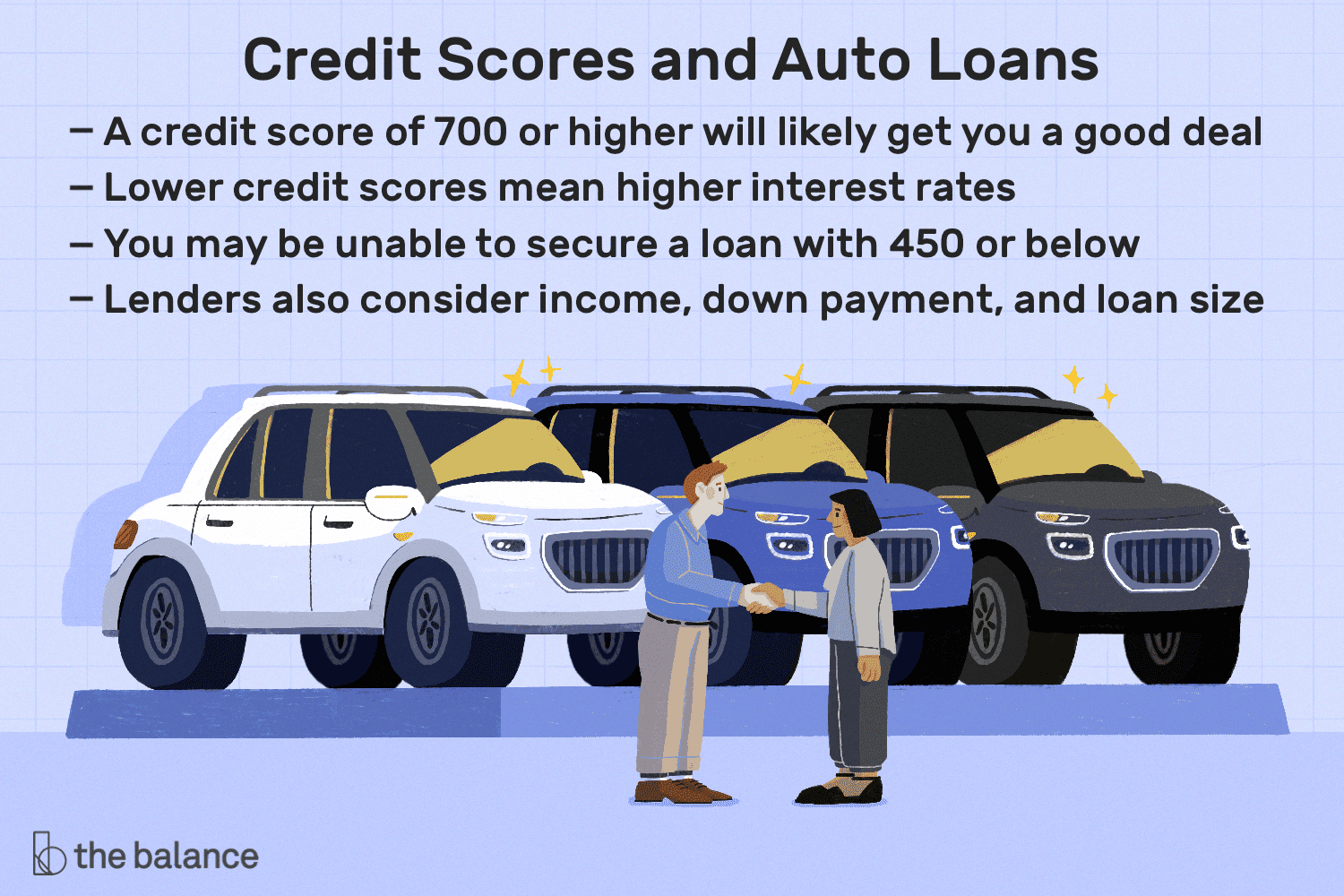

Applying your credit score to protected the ideal curiosity prices

By way of Experian

The all round purpose of the credit score score is common. However, unique loan companies in different sections of the entire world have their have requirements to measure an individual’s creditworthiness. When you utilize for an car bank loan in the US, the lender will run a credit history test as aspect of the procedure. The majority of the lending institutions use FICO credit history scores. This is a 3-digit score assigned to a borrower after the credit rating check work out.

It was originally made in 1989 by a facts analytics corporation known as Truthful Isaac Corporation. These days, there are a lot of variations of the FICO algorithm (and other scoring models, for that make any difference), but they are all aimed at ascertaining the borrower’s means to consider on credit score.

By means of The Harmony

In accordance to the CFPB (Purchaser Financial Safety Bureau) Purchaser Credit rating Panel, there are 5 unique borrower profiles sorted into the subsequent credit rating score buckets: Super-primary (720 & previously mentioned) Primary (660-719) Around-primary (620-659) Subprime (580-619) Deep subprime (beneath 580). A borrower with a rating under 660 can still secure vehicle financial loans, but they will be additional high priced than a Prime or Tremendous-primary borrower with a rating north of 661. The logic listed here is that you will want to preserve your credit rating score as high as attainable to get the greatest promotions when buying for vehicle financial loans.

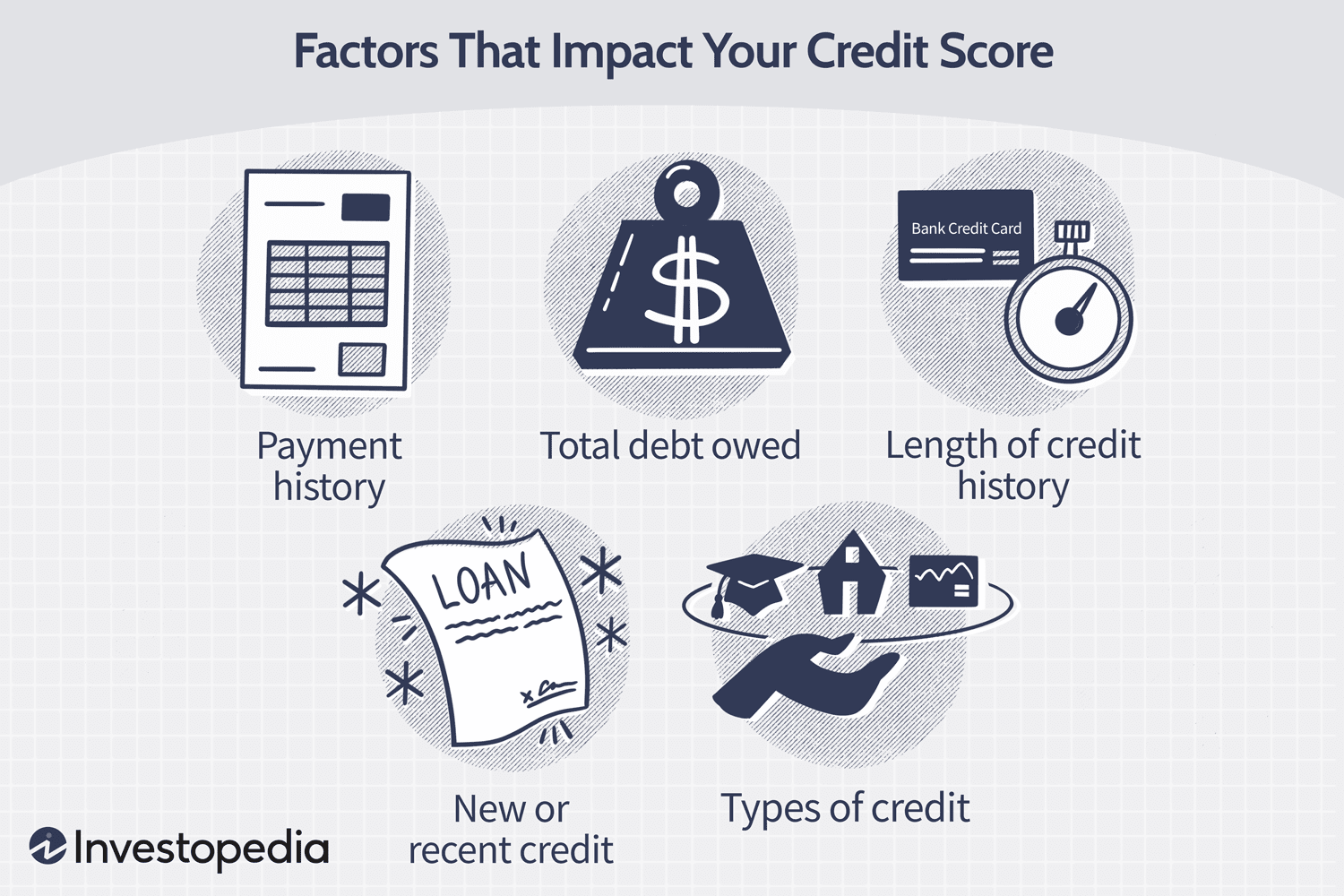

Points that hurt your credit rating rating

Through Investopedia

An exceptional credit score score is the result of watchful and deliberate setting up, and realizing the opportunity pitfalls can aid the borrower avoid generating missteps that pull down the rating into undesired territory.

Making a late payment

Payment history on your credit rating obligations accounts for up to 35% of the FICO rating. In accordance to FICO, a payment that is 30 times late can cost an individual with a credit history score of 780 or increased everywhere from 90 to 110 factors. It is crucial to make payments as at when owing and proactively attain out to the loan company if, for any explanation, payment will be delayed.

A significant credit card debt-to-credit score utilization ratio

Credit rating heritage is built by a regular cycle of credit rating utilization and shell out downs. Having said that, you will want to preserve an eye on the proportion of your debt load to general credit score. The lower your balances relative to your complete offered credit score, the better your score will be.

Non-utilization of credit

On the other hand, no credit record for an extended time period can also adversely have an effect on the borrower’s credit history rating. Loan providers and lenders have nothing to report to credit rating bureaus when you don’t utilize your credit rating accounts. This can make it additional demanding to assess future financial loan programs.

Individual bankruptcy

Filing for personal bankruptcy has a person of the most sizeable impacts on your credit history score. It can wipe as significantly as 240 details from an individual’s score, and what’s a lot more? A individual bankruptcy report can keep on the credit history heritage for up to 10 several years.

This list is by no usually means exhaustive, and other variables these as frequency of credit history purposes, credit rating card closure, cost-offs and refinancing all influence credit score scores in various levels.

Enhancing your credit history rating

Strengthening your credit score rating will entail preventing the pitfalls before determined above. Methods such as prompt and common invoice payments, protecting a low personal debt-to-credit history utilization ratio (ideally about 30%), trying to keep credit history card accounts open up and keeping away from various bank loan purposes at at the time are all measures in the proper path.

Having said that, even with all these ‘building blocks’ in area, a fantastic credit history score is not instantaneous. It may possibly consider a while to see any improvement, especially considering the fact that damaging reviews can continue to be on your credit history background for a number of yrs. There is no rigid time frame for credit history rating development as every single person’s economical situation is exclusive. In accordance to Forbes, it could take anywhere from a thirty day period to as a lot as 10 a long time. Of course, this is affected by aspects these kinds of as the individual’s present-day credit history standing and amount of money of whole exposure.

Securing automobile financial loans irrespective of credit history rating

By means of Geotab

A substantial credit rating will undoubtedly improve your possibilities of securing car funding and locking up the most effective curiosity rates. On the other hand, it’s not all doom-and-gloom for prospective automobile buyers with weak scores as they are not entirely with no solutions.

Irrespective of your credit history rating, searching close to and taking into consideration the many funding alternatives is really encouraged. It is just like browsing for the automobile alone an common buyer will evaluate unique dealerships and negotiate vigorously just before making the closing final decision.

Banks are the traditional resources for obtaining a loan, but you may be proscribing your alternatives if they are your only thought. Don’t overlook choice creditors. Working with third-celebration financing companies, these kinds of as getting your car bank loan by using LoanCenter.com, might give you with favourable desire premiums or funding conditions.

It is important to observe that only acquiring vehicle-mortgage preapprovals (various from genuine personal loan applications) although browsing all around will not affect your credit rating score because most scoring types do not handle this as a really hard enquiry.

In summary, a weak credit score score may perhaps press the least expensive interest rates out of achieve. On the other hand, obtaining a number of solutions will increase your odds of getting a deal with an interest fee that suits in your spending budget and permit you to invest in your wished-for vehicle.

[ad_2]

Resource connection

More Stories

The Ultimate Work Desk Kit: From Eye Drops to Vicks Roll On

Essential Insights into Atlanta Insurance: Your Ultimate Guide

Transform Lives by Giving Plasma: A Comprehensive Guide